")

Realty Income’s Higher Dividend Generate Tends to make It A Precious Expense (NYSE:O)

Table of Contents

Zephyr18

Realty Revenue (NYSE:O) has observed its share selling price fall virtually 10% YTD along with an practically 15% fall from its highs for the year. The firm’s dividend yield has pushed up to additional than 5% and the corporation maintains its position as the developing regular dividend firm. As we will see through this posting, the organization has the potential to carry on giving funds stream and escalating.

Realty Earnings Overview

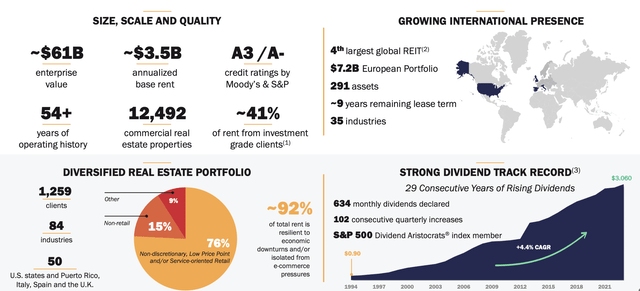

Realty Earnings has an in depth portfolio of assets, with a $40 billion industry capitalization and a $60 billion company value.

Realty Income Investor Presentation

The firm’s annualized base hire is $3.5 billion, which is roughly 9% of its portfolio. The enterprise has a multi-10 years running history with much more than 10 thousand properties and a A3/A- credit score ranking. The corporation is the 4th major global REIT, and has created up a >$7 billion European portfolio, an region with sizeable growth likely.

The company’s portfolio is effectively diversified and the enterprise has a lengthy dividend growth record. That transfers to sturdy dividend progress of far more than 4% annualized. Mixed with a a lot more than 5% dividend, which is an just about 10% annualized progress rate.

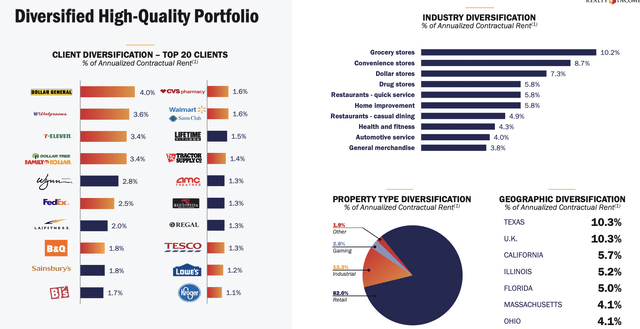

Realty Profits Diversified Portfolio

The firm’s portfolio is also very perfectly diversified by marketplace, although through significant black swan activities such as COVID-19, fears do come up.

Realty Income Trader Presentation

The firm’s greatest customer is Greenback Normal at 4% of income with Walgreens and 7-11 rounding out the best 3 for just above 10% of revenue. The company’s biggest segment is grocery suppliers, but the business is also greatly dependent on a selection of economic downturn resistant industries. By geography the corporation is effectively diversified with Texas as its most significant market place.

The firm’s diversification protects it, but with a significant downturn / recession, it is really nonetheless in a risky place.

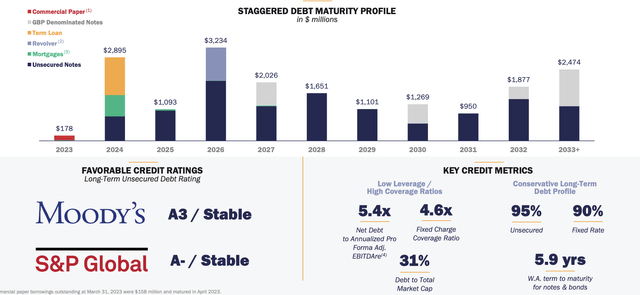

Realty Revenue Equilibrium sheet

The firm’s equilibrium sheet continues to be solid and staggered which minimizes chance.

Realty Profits Investor Presentation

The firm’s 5.4x web credit card debt to altered EBITDA is a degree that it can easily pay for. At the identical time, the company’s 31% personal debt to marketplace cap ratio and 5.9 12 months time period show its fiscal power. Its credit card debt is easily manageable compared to its equity and its expiration timeframe partly protects it from soaring curiosity rates. The business is at 90% fastened level.

The company’s 2023 credit card debt because of is small but in 2024, it has almost $3 billion due. That implies it’s going to need a partial debt rollover. In 2026, the firm’s maturities are much more than $3 billion. The firm’s in the vicinity of-expression debt obligations could perhaps lead to some climbing curiosity payments.

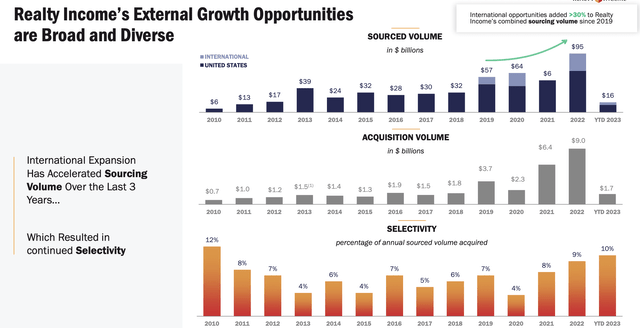

Realty Earnings Advancement Probable

The firm’s economical position allows continued development with investments.

Realty Revenue Trader Presentation

The firm has continued to supply $10s of billions of alternatives, with a sizeable selection of worldwide options. The business has remained selective with a single-digit selectivity rate. It’s continued to devote billions across a wide range of chances, but its selectivity charge has long gone up, which indicates that the company is maybe decreasing its requirements.

Continue to, as extensive as the company can go on to come across inexpensive investments that meet up with its standards, it can keep on its general advancement. That development likely will enable ongoing shareholder returns.

Our See

The company’s measurement permits significant further prospects. The firm’s Encore Boston transaction in December 2022 for $1.7 billion is an case in point of that. The sale-leaseback at a 5.9% cap rate comes with a 30Y lease phrase and 1.75-2.5% CPI will increase based on what inflation premiums are.

The raise in the company’s cap amount will guide to a lot more alternatives in the coming years, in our perspective, that have thrilling extended-term prospective. The business has a manageable credit card debt portfolio with a 5.9 year phrase that a little bit guards it from climbing curiosity charges. That will empower its cash move to develop in forthcoming quarters.

Placing it all with each other, the firm has a dividend of more than 5% that’ll permit escalating shareholder returns.

Thesis Threat

The major possibility to our thesis is the company’s valuation and earnings. The business has a dividend produce of just above 5%, but ordinarily we seem for a double-digit produce when investing. The enterprise is continuing to spend nevertheless, you can find no guarantee that its investments will crank out the expecting returns producing it a riskier expenditure.

Conclusion

Realty Money has an amazing portfolio of property. The firm has a dividend generate of more than 5%, which it pays every month, and it is continuing to guideline for mid-solitary digit dividend investments, which it can comfortably manage. Also, the enterprise is continuing to expand internationally, bringing in considerable extra prospects.

The firm’s sizing and scale makes it possible for it to convey in new opportunities these types of as the Encore Boston offer. At the exact same time, the firm’s general cap fee is escalating from rising interest prices, enabling the firm to lock in lucrative very long-term deals. The company’s credit card debt and higher valuation have some hazard, but overall we hope robust returns to continue.