")

Verizon Stock: Anatomy Of A Failing Commodity-Utility Investment (VZ)

Table of Contents

Huang Evan

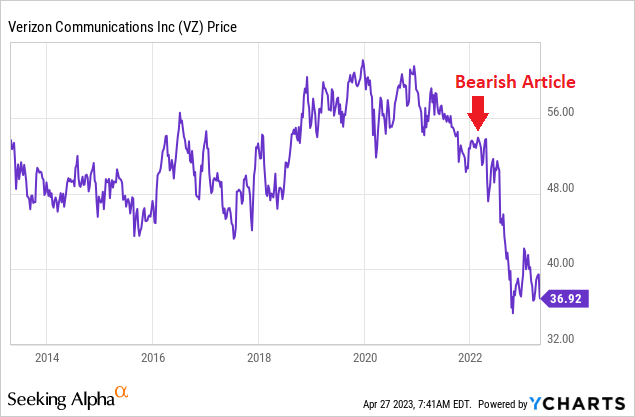

I wrote about Verizon Communications (NYSE:VZ) and its bearish fundamental future about a year ago in June here, explaining how weak sales and rising debt have not mixed well for business worth historically. I warned with price hovering around $50 a share, any slowdown in the economy would force earnings to stop growing and start the clock on potential dividend cuts. And, my concerns proved very timely. The share quote has backpedaled -27% over the last 11 months, with Wall Street analysts and investors becoming more nervous about Verizon’s long-term outlook on an economy sliding toward recession.

YCharts – Verizon, Price Changes, Author Reference Point, 10 Years Seeking Alpha – Paul Franke, Verizon Article, June 5th, 2022

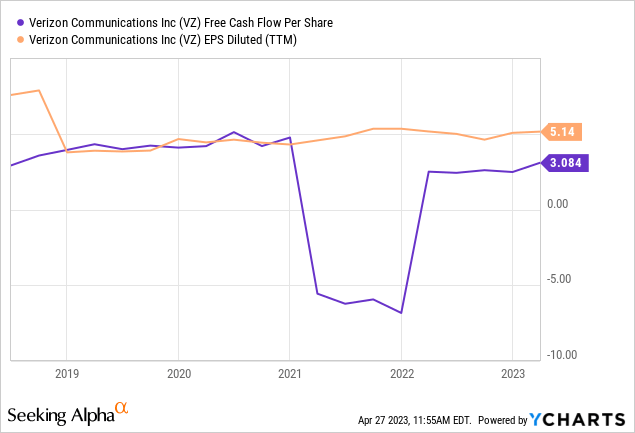

With high capital spending levels for 5G buildout still necessary to stay competitive, and rising interest rates in the economy eventually increasing company expenses, a real squeeze on free cash flow and earnings could be next into 2024-25. Already, both free cash flow and EPS have drifted into descending trends since 2018.

YCharts – Verizon, Free Cash Flow and Earnings per Share, 5 Years

For sure, a severe recession shock to wireless demand would cause a significant price war, slashing the topline and crushing earnings at Verizon. Under this scenario, the current VZ stock quote hovering around 10-year lows could dive toward 40-year lows closer to $25. Don’t say it cannot happen!

Performance Review

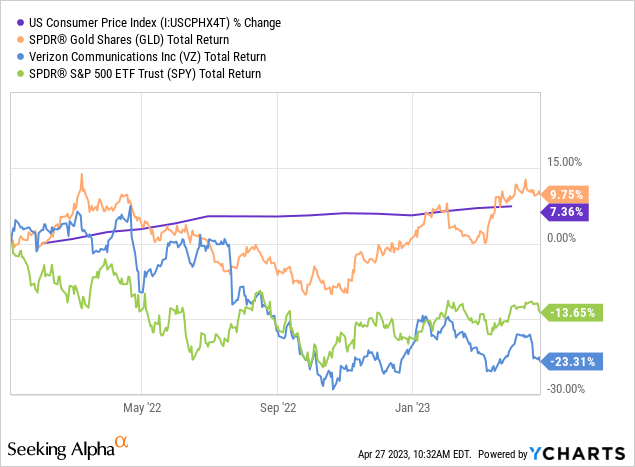

The first mistake many Verizon owners make is believing this utility-like investment is a great defensive play with above-normal dividend income characteristics. That’s not exactly how things have worked out the last decade. In fact, gold buried in your backyard has turned in a stronger buy-and-hold return! I know saying such will hurt a lot of feelings, especially from the Wall Street cult-followers watching CNBC and reading the Wall Street Journal, but here’s the truth.

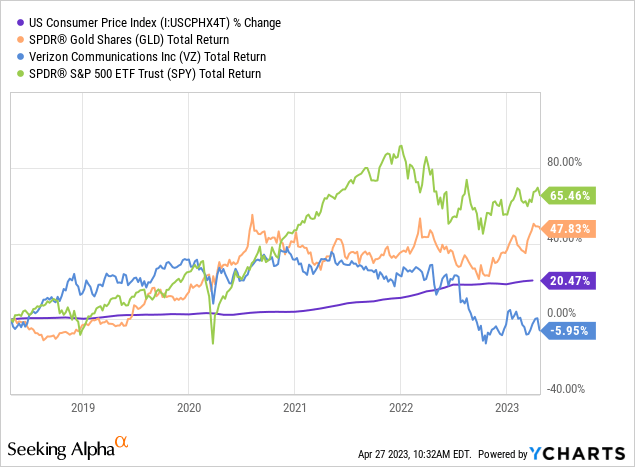

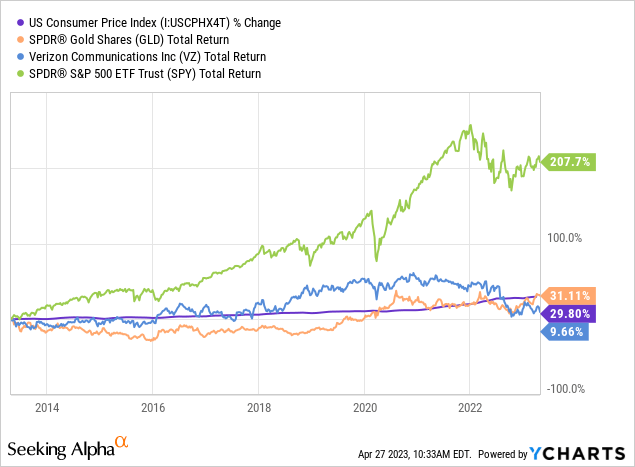

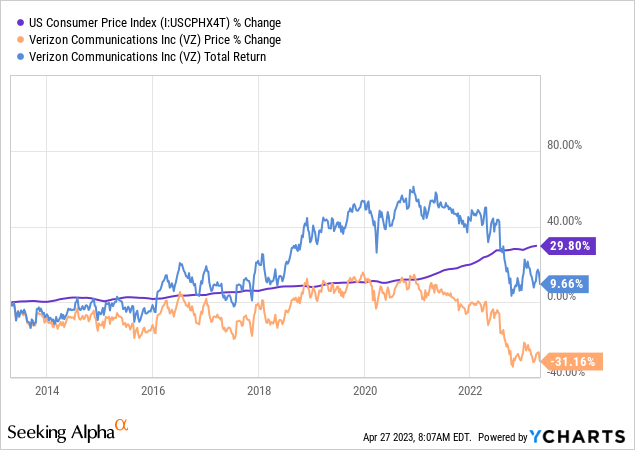

Reviewing stats since the U.S. equity bear market began in January 2022, or looking at 5-year and 10-year charts, gold bullion represented by the SPDR Gold ETF (GLD) has easily beaten the total returns, including dividends, outlined by Verizon. And, as a stock investment, just plucking down your capital into a plain vanilla, indexed SPDR S&P 500 ETF (SPY) has run circles around the lagging and now losing Verizon setup. To boot, and even more damning for realists, Verizon cannot even keep up with basic CPI inflation increases anymore.

YCharts – U.S. CPI vs. Verizon, Gold, S&P 500 – Total Returns, Since January 1st, 2022 YCharts – U.S. CPI vs. Verizon, Gold, S&P 500 – Total Returns, 5 Years YCharts – U.S. CPI vs. Verizon, Gold, S&P 500 – Total Returns, 10 Years YCharts – U.S. CPI vs. Verizon, Price Only & Total Returns, 10 Years

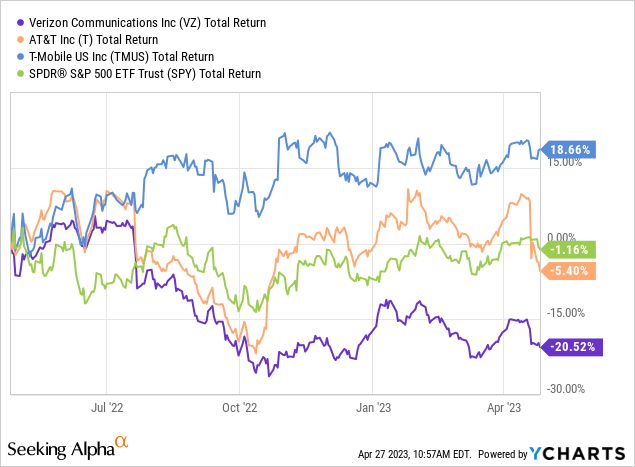

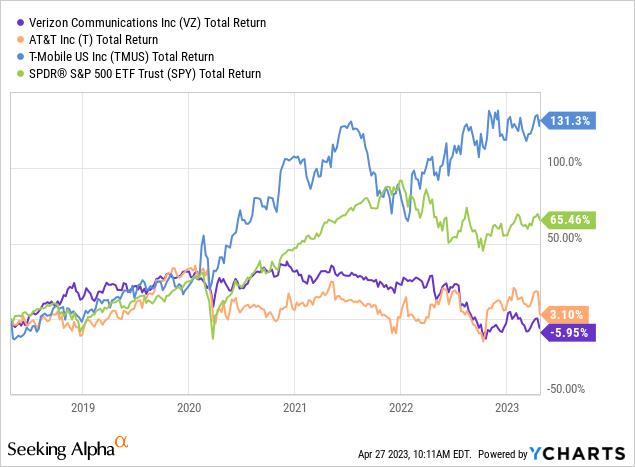

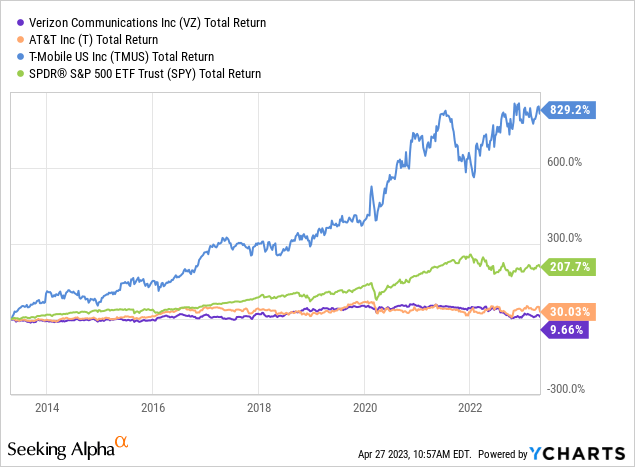

More bad news for investors, Verizon has been the weakest to own of the Big 3 wireless carriers. When we compare VZ performance to closest competitor AT&T (T) or newcomer T-Mobile US (TMUS), existing shareholders have plenty to complain about. Essentially, Verizon has been an investment failure across the board over the last decade. I have charted total returns from each over 1 year, 5 years, and 10 years below.

YCharts – Verizon vs. AT&T, T-Mobile, S&P 500 – Total Returns, 1 Year YCharts – Verizon vs. AT&T, T-Mobile, S&P 500 – Total Returns, 5 Years YCharts – Verizon vs. AT&T, T-Mobile, S&P 500 – Total Returns, 10 Years

Weakening Financials

The primary reasons for this rotten performance are (1) serious competition in the wireless market has prevented price increases beyond rates of inflation for many years, and (2) Verizon is honestly carrying extraordinary debt needing to be serviced, while its business model requires even greater capital spending to stay competitive in the new 5G marketplace.

Then, two negative economic turns in 2022-23 have conspired to cause a rethink of the company’s future by analysts and investors. Rising interest rates, affecting the long-term debt cost of doing business, and now a slowing economy with all kinds of bearish repercussions for wireless demand and pricing have come to the fore. I warned about this developing situation last year.

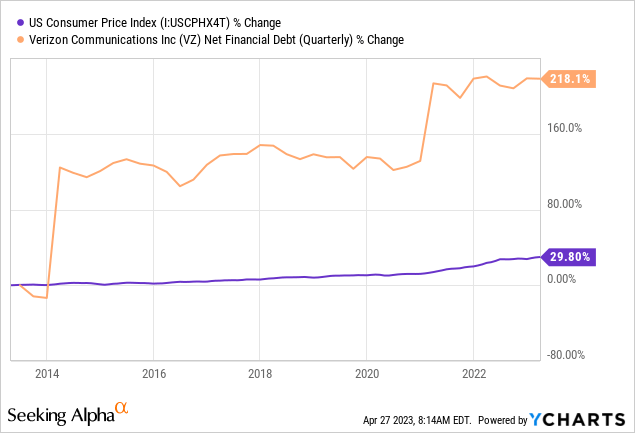

One variable out of Verizon’s financial setup that has grown at rates well above CPI inflation is debt/leverage. Over the last decade total debt has more than tripled.

YCharts – U.S. CPI vs. Verizon Debt Changes, 10 Years

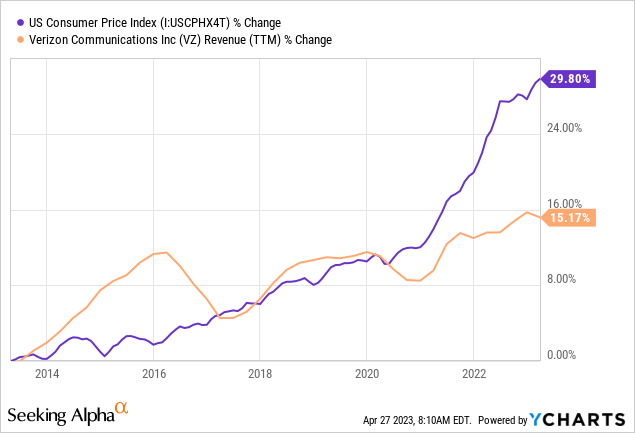

The debt service squeeze on margins would not be material if underlying sales had grown as hoped from acquisitions, 4G and 5G rollouts, and industry growth with the consumer adoption of smartphones. Nevertheless, revenues have been stagnating over the whole 10-year period. Sales (and sales per share) have only risen at half the rate of inflation! This combination of weak sales and rising debt is often a horrible development for equity value.

YCharts – U.S. CPI vs. Verizon Revenue Changes, 10 Years

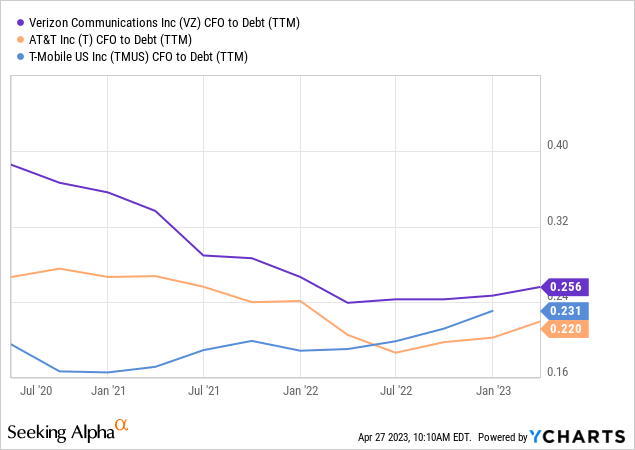

Over the past three years, accounting cash flow generation as percentage of rising debt has been crashing. This ratio is down almost 40% from 2020. And, this rapid decline in relative efficiency and productivity has been a bigger hit than witnessed at AT&T and T-Mobile. T-Mobile’s cash flow to debt has actually improved over the same span.

YCharts – Verizon, AT&T, T-Mobile, Cash Flow to Debt Ratios, 3 Years

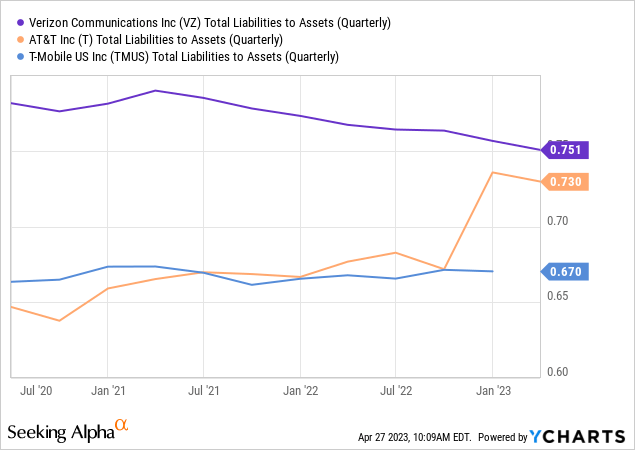

More bad news, total liabilities to assets remain higher than either AT&T or T-Mobile. Although slight improvement in this ratio has been accomplished since 2020, Verizon’s $150+ in total debt remains one of the highest of any single company in the world.

YCharts – Verizon, AT&T, T-Mobile, Total Liabilities to Assets, 3 Years

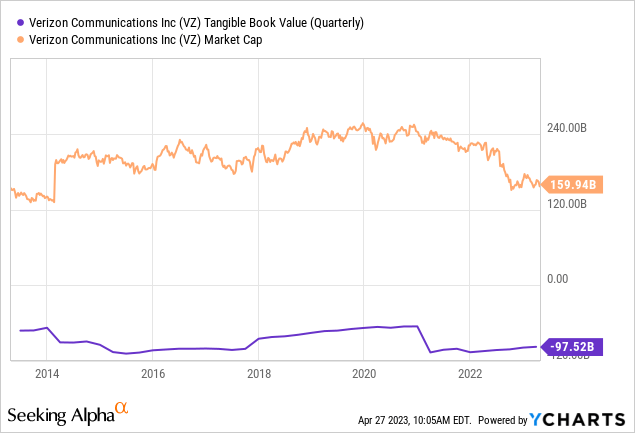

And, a huge chunk of “assets” on the balance sheet are related thin-air accounting. You heard me right. Intangible assets for wireless licenses and goodwill on asset purchases are not the kind you can touch or potentially resell at face value easily in a wireless industry downturn.

I try to avoid companies with large negative “tangible” book values. Verizon again has one of the worst hard-asset book values in the world, today sitting at a negative -$97 billion! If you add this sum to Verizon’s current $160 billion in equity capitalization, what appears to be a cheap valuation on trailing earnings and cash flow, really isn’t. In my view, this is the only fair way to evaluate investment propositions against other companies with material tangible book value backing up your capital.

YCharts – Verizon, Equity Capitalization and Tangible Book Value, 10 Years

Final Thoughts

I know Verizon is paying a solid 7% dividend yield presently, and income investors love the name. However, if your total return fails to keep pace with general inflation the next 3-5-years, as the share price slides further and overburdened debt loads slash business returns, safer defensive investments like gold and other dividend compounders will be a smarter place to park your money.

I rate Verizon an Avoid to Sell for most readers. To me, it is turning into a classic “value trap,” where low trailing valuations on business results make it look inexpensive for new buyers. In the end, minor single-digit total returns to continued losses will not stack up well with our new long-term inflation rate of 4%+ annually. In my research, the only way U.S. inflation comes down from today’s 5% core-rate is through a major recession, which could decimate Verizon earnings and sales. It’s really a “be careful what you wish for moment” in the stock market overall.

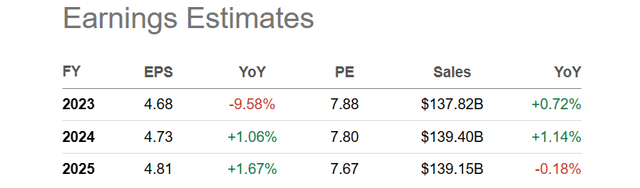

For me, current Wall Street projections for earnings and sales into 2025 represent a best-case scenario of decent economic growth in America, with falling interest rates, and some pricing power at the Big 3 wireless giants. If any of these pillars crumble, the dividend payout rate of $2.61 could quickly be put into serious jeopardy. In a severe “stagflation” recession, with rising interest rates, earnings under $2 per share are not impossible to model as the new normal for Verizon a few years out (using a price-war sales decline of -10% alongside gradual annual +5% to +10% increases in labor and debt-service expenses).

Seeking Alpha Table – Verizon, Analyst Estimates for 2023-25, Made on April 26th, 2023

Too much debt leaves this company stuck in a low-growth profile at best. Readers explained to me debt wasn’t a problem in last year’s article, because low interest costs were largely locked-in for a few years. I agree, without this setup, Verizon would likely be much lower in price right now. The cold truth is eventually the company will have to refinance at much higher rates in coming years, and Wall Street is starting to discount this fact.

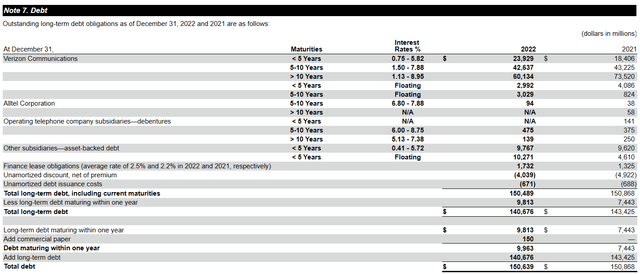

$48 billion of debt held at the end of 2022 was maturing over 5 years or less, another $42 billion between 5-10 years out, and $60 billion beyond 10 years. In other words, if interest rates do not reverse lower soon, total interest expense on past debts is now entering a rising trend long term on higher refinance rates. Plus, new debt issued to build out and upgrade its networks will be done at far greater expense than the recent past.

Verizon – 2022 10-K Filing, Debt Schedule

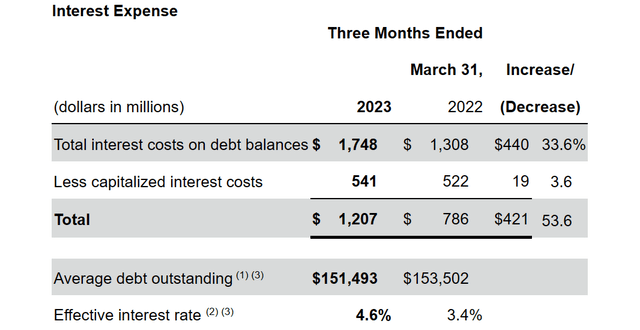

The Q1 2023 earnings report out this week lists a material rise in overall interest expense of $421 million for the three months between January-March vs. 2022’s equivalent period, good for a jump of +1.2% in effective rates on past debt spending.

Verizon – Q1 2023, Interest Expense Table

Unfortunately, Verizon’s products have become something of a commodity and utility investment in one. No longer can investors count on a phone “monopoly” to generate stable to growing sales/earnings with inflation and economic advances in America. Today, Verizon has to deal with several large competitors and cheap-plan variations mandated through deregulation and lawsuit verdicts. Too much debt and price competition means the future for Verizon as a long-term investment is not worth my attention. Then, you get a recession that smashes the business valuation even lower. Really, that’s the best description of Verizon’s troubles in 2022-23.

How could the company transition into a better investment choice? At this stage, reducing debt through equity issuance and/or a major dividend cut to keep higher amounts of cash flow are the only ways forward. Of course, the initial Wall Street reaction to either would be an oversized share price drop. So, we’re left with a slow trickle decline in value like witnessed the past five years, or an all-at-once dump back to 40-year lows for price, before a stronger shareholder total return can be achieved.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.